Microsoft not going soft

Microsoft is going hard. An overview of Microsoft's current business and valuation estimates

Introduction

Microsoft is a company that has a wide moat, ranging from switching costs, network effects, and cost advantages. We view the company as a leader in across a variety of key technology areas, which we believe makes the business highly susceptible to generating economic returns way above the cost of capital. In its Q1 the company reported solid top-line and bottom-line results. This indicates modest improvements in the demand environment on the commercial side stemming from Azure.

What is the business exactly?

Productivity & Business Processes:

This unit represents 1/3rd of revenues & spans productivity, communication, and information products and services across devices and platforms. This business unit includes Office Commercial (Office 365 (the cloud version)), SharePoint, Skype, Microsoft 365 Consumer subscriptions, the Dynamics ERP and CRM products + LinkedIn.

Key structural change for this business unit is the shift from traditional on-premises products to become cloud-based SaaS solutions. When it comes to LinkedIn, Office 365, Dynamics 365 and the Power platform, these moves are beyond the halfway point and no longer a financial drag.

Microsoft’s productivity & business processes segment has established a particularly wide moat. Office 365 and the perpetual license version is a highly protected business with a moat driven by high switching costs and networking effects. To put it simply, you cannot access our financial model if you do not use Excel and because we used Excel for it you and your friends will do so too. In addition, both products to date are growing in the low double-digit area:

The office productivity suite for the usual user generally consists of Excel for spreadsheets, word processing with Word and PowerPoint for presentations. Other additional applications can also be bundled in as MSFT offers a variety of versions of the Office 365 Suite, and increasingly fewer perpetual license versions. Office 365 starts at approximately $6 per month and tops out at approximately $35. With education becoming more accessible, lower-cost and even free versions are available for students and educational institutions, further assisting the wide moat by conditioning customers from early on.

The fact that a substantial number of users consistently opt for the paid Office 365 subscription, priced at a minimum of $70 annually, despite the availability of free alternatives that offer comparable features and user interfaces, is a testament to Microsoft's formidable pricing power. This willingness of users to pay for Office 365, even in a market where no-cost options exist, strongly underscores the company's robust market positioning and reinforces our conviction in its wide economic moat. This scenario not only reflects the high value users place on Microsoft's offerings but also illustrates the company's strategic efficacy in differentiating its products and fostering brand loyalty.

The moat of this business is also grounded in the fact that Microsoft was a first-mover in office software. This allows the company to continue enjoying a dominant market share while other players like Google with Drive, Apple’s iWork, Apache OpenOffice, and others are the remnants of a market still in the above-average returns, growth territory that has a winner-takes-most dynamic because of the high switching costs and network effects inherent in the product.

When it comes to dissecting the strong networking effects, the financial system CANNOT survive without Excel, so much so that many products are built in mind to work well with Excel. For instance, the Bloomberg Terminal Excel add-ins and more.

Intelligent Cloud:

This segment accounts for over 40% of revenue, consists of its public, private and hybrid server products and cloud services headlined by Azure cloud computing service. Other products and services include SQL Server, Windows Server, Visual Studio, System Center, and related Client Access Licenses (CALs), Nuance, and GitHub.

Azure is the centerpiece of the new Microsoft. Even though we estimate it is already an approximately $58-billion business, it grew at an impressive 30% rate in fiscal 2023. Azure has several distinct advantages, including that it offers customers a painless way to experiment and move select workloads to the cloud creating seamless hybrid cloud environments. Since existing customers remain in the same Microsoft environment, applications and data are easily moved from on-premises to the cloud. Microsoft can also leverage its massive installed base of all Microsoft solutions as a touch point for an Azure move. A massive structural advantage. Azure also is an excellent launching point for secular trends in AI, business intelligence and Internet of Things, as it continues to launch new services centered around these broad themes.

“Azure becoming the centerpiece of the new Microsoft”

Considering this transformation of Microsoft, it is worthwhile to mention that before taking on the role of a CEO, Satya Nadella was EVP of Microsoft’s Cloud and Enterprise group. As evident by the performance of the unit, Satya. In this role he led the transformation to the cloud infrastructure and services business, which outperformed the market and took share from competition. The company he took over is very different than the company we see today, and the transformation has been nothing short of dramatic. We remain confident in Nadella’s strategic vision to carry Microsoft forward.

What allowed Microsoft to integrate horizontally across every bit of software infrastructure was its early presence in the PC market with both its OS and Office productivity software. Today this allows for Microsoft’s unique ability to seamlessly move clients from an on-premises Microsoft environment to a count Microsoft environment via Azure. The cloud theme is evolving and IT environments are predominantly hybrid-based underlying the necessity for flawless migration of workloads.

Additionally, this early lead and profound market share have helped the company develop a sizeable developer community joining the ecosystem bringing in applications, middleware, and development tools. This creates a flywheel effect where more developers help attract more customers and more customers attract more developers.

More Personal Computing:

The "More Personal Computing" segment of Microsoft represents a diversified portfolio, crucial for its strategic positioning in the dynamic tech market. This segment encompasses:

Windows Operating System Products: A foundational element, Windows OS is pivotal in personal and enterprise computing, establishing Microsoft's dominance in software ecosystems.

Devices: Including the Surface series and HoloLens, these devices showcase Microsoft's innovation in hardware, integrating seamlessly with its software offerings, while marking its presence in the premium device segment.

Gaming: Encompassing Xbox hardware and services like Xbox Game Pass and Xbox Cloud Gaming, this division places Microsoft at the forefront of the evolving gaming industry. The focus on subscription models and cloud gaming aligns with current industry trends and consumer preferences.

Third-Party Disc Royalties and Advertising: This area, though smaller, diversifies revenue streams through licensing and advertising via Bing and MSN.

Activision Acquisition: This strategic move is set to significantly enhance Microsoft's gaming portfolio, expanding its reach into mobile gaming and potentially into burgeoning areas like virtual environments.

Investment Thesis

Noncyclical business supported by a secular tailwind in AI and Cloud.

Microsoft is one of the 3 public cloud providers that can deliver a wide variety of PaaS/IaaS solutions at scale. Based on its investment in OpenAI, the company is emerging as one of the leaders in the AI arms race. Additionally, the company has enjoyed great success in upselling users on higher priced Office365 versions. This combination and cohesiveness across products facilitates the deliverability of consistent highly defenisable growth at high margins.

Expanding on the partnership with OpenAI, earlier in 2023, Microsoft continued to extend its exclusive partnership with OpenAI along with an increase in investment in supercomputing and integration of generative AI while being the one and only cloud provider of the most influential invention to your university assignment. Through the announcement of homemade AI chips, Microsoft continued to strengthen its position in the AI war and acquire a first-mover advantage in capitalizing on generative AI demand as well as mitigating the dependency on its chip provider, Nvidia. The new AI chip, Maia 100, is customised for AI processing and tailored for LLM and will be used for Bing and various copilot features. This innovation aids Microsoft in launching its latest model-as-a-service allowing clients to build their own large language model using third-party models.

As mentioned earlier, we view Azure as the centerpiece of the new Microsoft. Azure has been continuously the main revenue driver for Microsoft, consistently registering growth of 30%+ over the course of the last couple of years. The platform's primary strengths lie in its ability to facilitate a smooth transition for customers looking to migrate select workloads to the cloud. It excels in creating integrated hybrid environments, thereby reducing friction for users transitioning from on-premises to cloud infrastructures. Microsoft's expansive installed base across its various solutions provides a strategic advantage, serving as a natural springboard for clients considering a shift to Azure. The platform is adept at capitalizing on key secular trends, including AI, business intelligence, and the Internet of Things. Azure’s ongoing development and launch of new services in these areas not only reinforce its market leadership but also demonstrate its commitment to innovation and meeting evolving customer needs.

Microsoft's expansive installed base across its various solutions provides a strategic advantage, serving as a natural springboard for clients considering a shift to Azure. The platform is adept at capitalizing on key secular trends, including AI, business intelligence, and the Internet of Things. Azure’s ongoing development and launch of new services in these areas not only reinforce its market leadership but also demonstrate its commitment to innovation and meeting evolving customer needs. As such, relative to peers AWS and Google, Microsoft possesses great focus on verticalization of cloud revenues that are highly defensible and growing:

Our perspective on holding Microsoft stock transcends the conventional objective of capital appreciation. We perceive it as embodying a strategic role within an investment portfolio, akin to a call option on AI. This viewpoint is grounded in the anticipation of emerging business models through Microsoft's collaboration with OpenAI, coupled with the expansion of its cloud business. Furthermore, the integration of AI applications into Microsoft’s existing suite of Office products presents a significant value-addition, reinforcing the stock's potential as a leveraged play on the future advancements in AI technology.

Cloud Market Outlook

To better understand the competitive landscape surrounding Microsoft, we need to examine the three pillars of the cloud industry: Infrastructure-as-a-Service (IaaS), Software-as-a-Service (SaaS), and Platform-as-a-Service (PaaS). While Microsoft competes through Microsoft 365 suit and above market growth with even distribution between application (57%) and infrastructure (43%), AWS relies heavily on infrastructure products to generate 96% of its revenue.

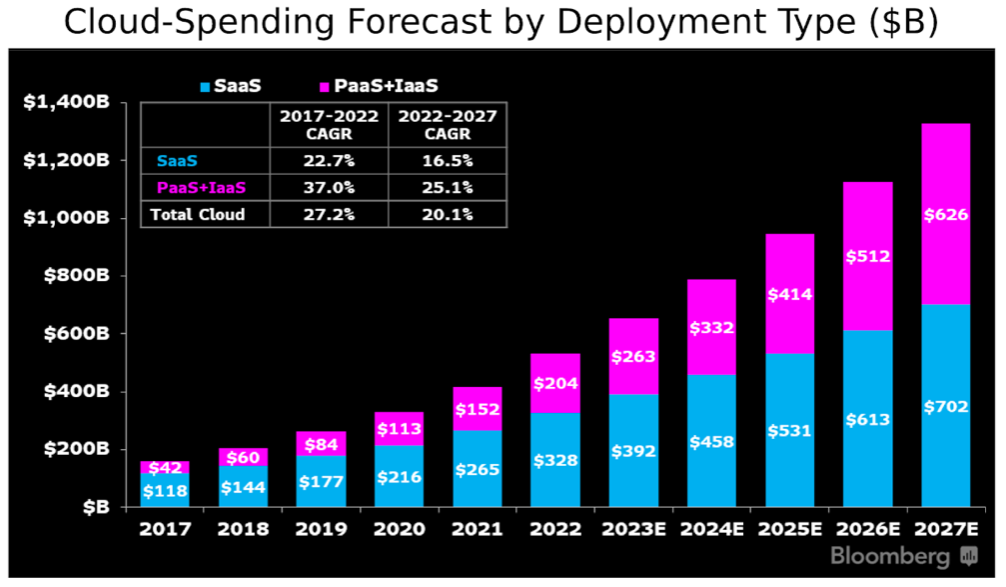

SaaS, accounting for 62% of total spending, is the largest market in the cloud industry. However, due to the shift to cloud infrastructure, SaaS has entered its mature stage, and growth is expected to be slower than the other two segments:

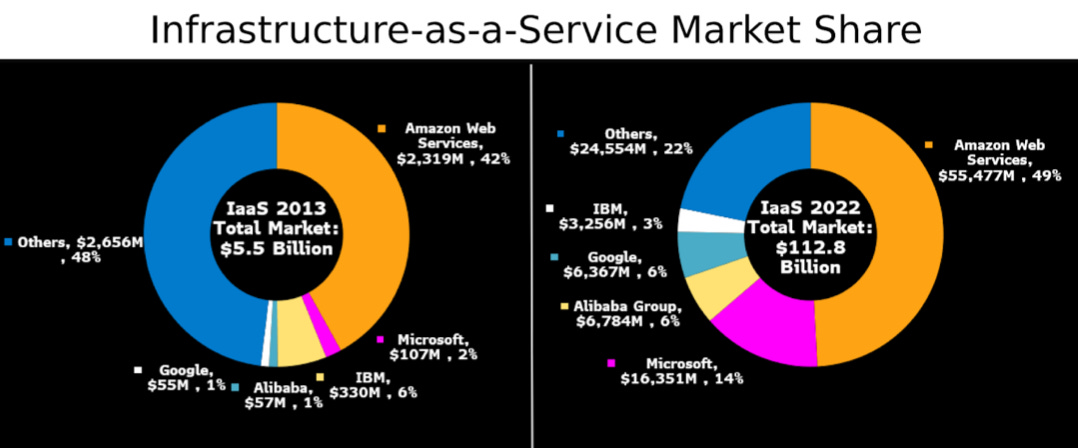

The IaaS market shows potential long-term growth for Microsoft and AWS aided by the development of AI; however, the short-term perspective remains uncertain due to the recession economy. In the long run, the consumption-based pricing models would initiate companies to shift to IaaS to reduce their IT spending. Currently, AWS remains the dominant player in this segment with a 49% market share. Despite having a slightly lower market share growth rate, with the integration of AI, Microsoft shows potential for further growth as they have a large on-premises consumer base providing a faster transition to a public cloud model:

Leveraging its large legacy footprint of server and database products, Microsoft has the potential to drive about 30% sales growth over the next two years, further closing the gap with AWS.

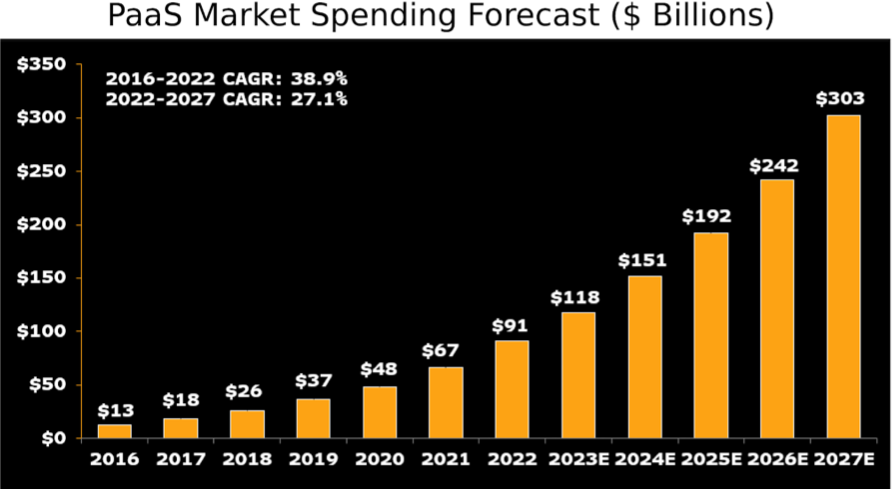

Finally, the PaaS market is estimated to expand significantly with the support of generative AI tools such as copilot driving the transition to cloud infrastructure, benefiting cloud providers. Microsoft currently maintains the leading position with a strong market share among corporate IT aiding further expansion. Dominating data management software, 44% of total PaaS spending, amplifies Microsoft’s growth within the cloud transition.

Risks

Following the blooming development of AI is the rising in cyber security risk, unethical issues and uncertainty in government AI regulation. Over-reliance on AI poses numerous obstacles in managing system and data safety, especially with this fast-paced growth, the global cost of cybercrime is estimated to reach 23.82 trillion USD in 2027. Being aware of this issue, Microsoft has unveiled its Security Copilot providing further data protection and end-to-end security. This major risk also brings up highly uncertainty in future AI regulation and legislation that Microsoft needs to carefully follow and take into account for future products and services.

On the other hand, the battlefield among the big 3 cloud providers (Google, Microsoft, and Amazon Web Service) remains fiercer than your investment banking career. With the latest release of Gemini AI model, Google is trying to get back into the race claiming that this model is even stronger and better than ChatGPT. Meanwhile, Microsoft maintains a more diversified product portfolio with strong edge in hybrid cloud and cloud migration, providing a first-mover advantage into AI integration compared to AWS. Through extensive R&D and better go-to-market capabilities and a more verticalized product stack, Microsoft is closing the gap on AWS in terms of IaaS.

Valuation

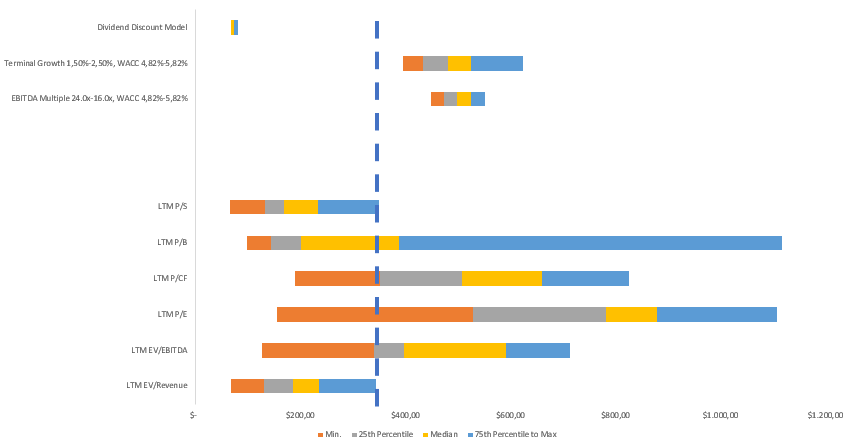

Relative to peers results are mixed. Microsoft trades at the higher end with regards to relative valuation. When it comes to the intrinsic valuation portion of the football field, most prices in our sensitivities are above the current share price as the company according to our estimates is trading significantly below our DCF values.

We are also accounting for the fact that Cloud is going to be the main revenue growth driver for the company:

Additionally, we are forecasting consistent margins at above 40%. The company has been historically able to perform at this level because of gross margin expansions through increases in pricing alongside tighter expense control. This leads us to believe that the company can adequately manage higher processing costs tied to AI workloads as the year progresses.

We view Microsoft’s capital allocation strategy centered around re-investing back into the business and we view those investments as the key drivers of shareholder value going forward. Therefore, we believe that funds being allocated as is are appropriately prioritized over the capital returns from dividends.

| A guest post by

|